Owning rental property can be rewarding, but understanding Rental Income Tax Rates is key to keeping your earnings on track. If you earn money from rent, you’ll need to know how much of your income goes to taxes and how to stay compliant while saving smartly.

What Is Tax Rate Determination?

The tax rate on rental income depends on how much you earn in a year and your overall taxable income. The IRS sees rent as part of your regular income, so it’s added to your total earnings before taxes are calculated.

If you’re wondering how much of rent income is taxable, the answer is simple — all your rental profits are taxable unless you have deductible expenses. You can deduct property repairs, mortgage interest, insurance, and property management fees. This reduces your taxable income and lowers your final bill.

In short, the higher your rental profit, the higher your rental income tax rate might be. But with good records and clear reporting, you can keep things under control.

Federal Tax Rules and How They Work

Your income tax on rental income usually follows your federal income tax bracket. That means if you fall into a 22% tax bracket, your rental income will also be taxed at that rate.

If you have multiple properties, keep track of each one’s income and expenses separately. Organized records can help calculate your rental profit tax accurately.

Here’s a quick example:

- You earn $18,000 a year in rent.

- You spend $5,000 on maintenance and property tax.

- You report $13,000 as taxable rental income.

That $13,000 adds to your annual income and is taxed at your personal tax rate.

State and Local Tax Considerations

Federal rules apply everywhere, but each state has its own tax treatment of rental property income.

In California, for example, rental income is taxed as part of your state income. Many property owners rely on bookkeeping service Los Angeles to manage local filings and avoid confusion.

If you own property in Utah, you’ll need to check rental taxes in Utah, as they have separate rates and regulations. Some cities might even have additional local charges. Always review both federal and state rules before filing your return.

Is Rental Income Taxed as Ordinary Income?

Yes, in most cases, rental income is taxed as ordinary income. It’s treated just like your salary or business income. This means you pay the same percentage of tax on it based on your tax bracket.

However, the difference is that rental property owners can claim deductions. These deductions help offset the tax percentage on rental income and reduce what you owe. Expenses like property management, advertising, and depreciation can make a big difference.

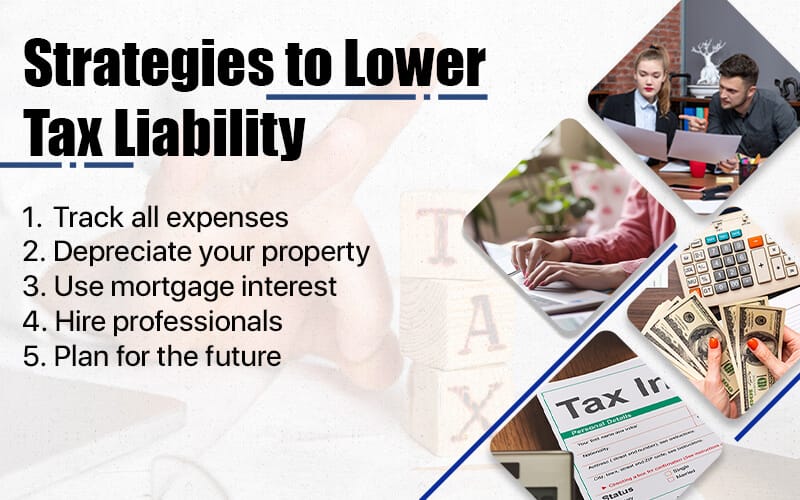

Strategies to Lower Tax Liability

Smart planning can help reduce your tax on rent income. Here are a few simple strategies:

- Track all expenses: Every repair, upgrade, and maintenance cost adds up. Keep receipts and invoices.

- Depreciate your property: The IRS allows annual depreciation deductions over several years.

- Use mortgage interest: You can deduct the interest portion of your loan payments.

- Hire professionals: Having an accountant or a property management service helps you stay compliant and find savings.

- Plan for the future: Setting aside part of your rental income for taxes avoids last-minute surprises.

These steps don’t just keep your rental income tax manageable — they also make your record-keeping easier at the end of the year.

What Are the Tax Rates on Rental Income?

There’s no fixed number since your tax rate rental income depends on your tax bracket. For most people, it ranges between 10% to 37% federally. On top of that, your state’s tax might add a few more percentage points.

If you ask what is the tax for rental income, the best answer is — it depends on where you live, how much you earn, and what deductions you claim. For example:

- A small property might face around 12%–22% total tax.

- A large property with higher income might reach up to 35%.

Keeping accurate reports helps you know where you stand before tax season.

Final Thoughts

Understanding Rental Income Tax Rates is part of being a smart property owner. It’s not just about paying taxes – it’s about managing your profits wisely, planning ahead, and keeping good records. Whether it’s organizing expenses or staying updated with local rules, you can always make your rental business smoother and stress-free.

For expert help with filing and planning, reach out to Jarrar CPA.

Must Read: Understanding California Estate Tax: What You Need to Know

FAQs

1. Do I have to pay taxes if I rent out my home for only part of the year?

Yes. Even if you rent your property for just a few months, that income counts as taxable. However, you can deduct expenses for that rental period, like cleaning or repairs.

2. Can I claim a loss on my rental property?

Yes, you can. If your rental expenses are higher than your rental income, that’s called a rental loss. Depending on your income level and situation, you might be able to deduct it from other taxable income.

3. How do I report rental income to the IRS?

You need to report it on Schedule E of your tax return. This form helps you list both your income and your deductible expenses related to the rental property.

4. What happens if I don’t report rental income?

Not reporting rental income can lead to penalties or interest from the IRS. It’s always better to declare all rental earnings honestly to stay compliant and avoid future issues.

5. Can I deduct travel expenses for managing my rental property?

Yes. If you travel to your rental property for inspections, repairs, or meetings with tenants, those travel costs may be deductible. Keep records of mileage, tickets, or receipts.

6. How long should I keep records for my rental property?

It’s smart to keep your records for at least three years after filing your tax return. This includes receipts, invoices, and proof of payments in case of audits.

7. Are security deposits taxable income?

Not right away. If you plan to return the deposit, it’s not taxable. But if you keep part or all of it to cover damages or unpaid rent, that amount becomes taxable income.

8. Can I split rental income with my spouse for tax purposes?

If both names are on the property title, yes. Each of you can report half of the income and expenses. This can sometimes help lower your overall taxable income.

9. What if my property is in another state?

You may need to file a state tax return where the property is located. Each state has its own rental income tax rules, so it’s important to check the specific state’s requirements.

10. Is there a limit to how many properties I can own before taxes change?

No fixed limit exists. But once you own multiple properties, your rental activity may be viewed as a business, changing how your income and deductions are handled.